The UK construction industry has hit its lowest point in six years, driven by a significant downturn in house building, according to the latest S&P Global UK Construction PMI data. This trend poses critical challenges for AECM professionals as they navigate the complexities of reduced tender opportunities and heightened input costs.

What Happened

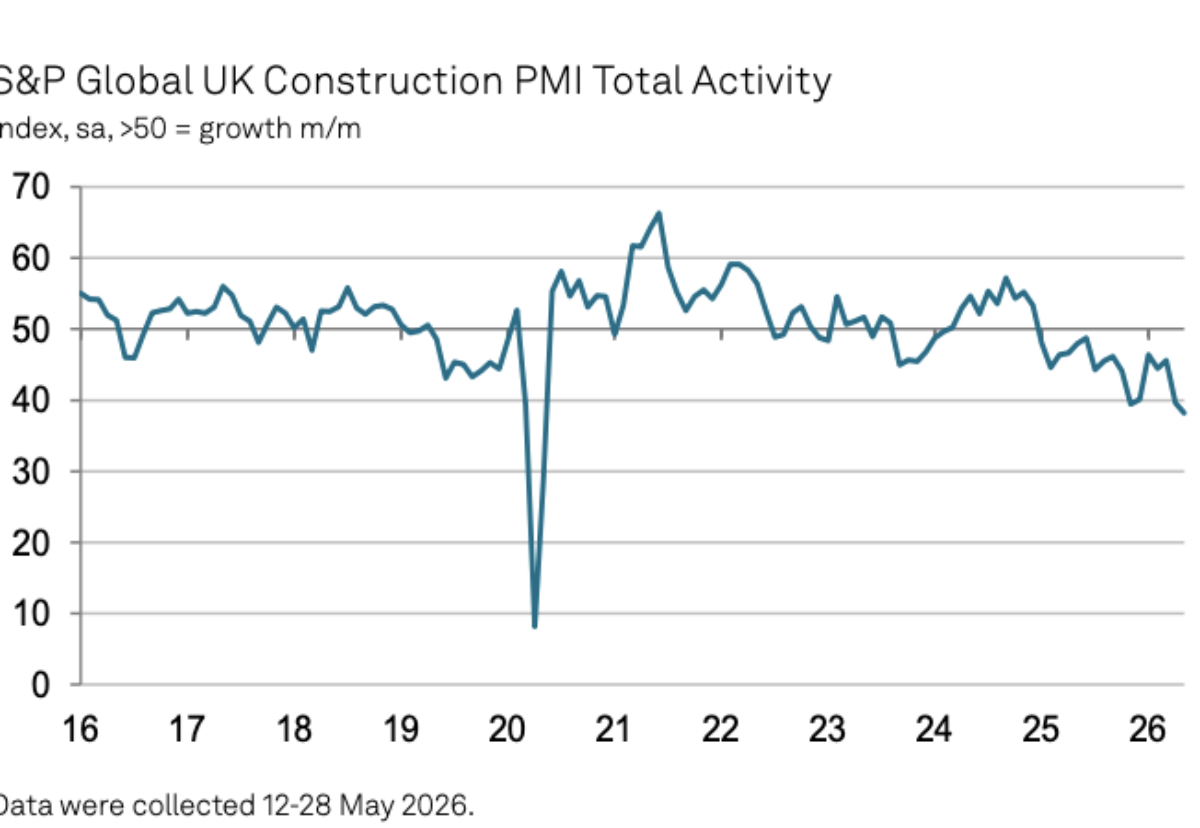

The S&P Global UK Construction PMI fell to 38.2 in May, down from 39.7 in April, marking the seventeenth consecutive month of contraction. This downturn is the most severe since May 2020, at the height of the pandemic, and outside of that period, it is the sharpest decline since March 2009. House building remains the weakest sector, with a residential activity index of 36.0. Commercial construction and civil engineering are also under pressure, with indices of 39.0 and 36.2, respectively. Contractors are facing the fastest fall in new work in six years, attributed to project delays, deferred investment decisions, and budget cuts. Political and economic uncertainties further exacerbate the situation. Despite these challenges, the energy sector offers a glimmer of hope, with upcoming power network and infrastructure projects providing opportunities.

Supply chain issues are worsening, with delivery times lengthening for the third consecutive month due to international shipping disruptions and material shortages. Input cost inflation has surged, with nearly two-thirds of firms reporting higher purchasing costs in May, driven primarily by fuel surcharges, energy bills, and transport costs.

What This Means for Your Business

For US AECM operators, the current UK construction downturn highlights the importance of strategic planning and risk management. Companies should be vigilant about cost management, especially as input prices rise sharply. The energy sector's continued investment in infrastructure projects could present opportunities for firms with expertise in this area. Additionally, the emphasis on understanding political and economic landscapes will be crucial in navigating market uncertainties.

Compliance with international trade regulations and adapting to supply chain disruptions will also be pivotal. US operators with interests in the UK market need to be prepared for potential delays and increased costs, ensuring robust contingency plans are in place.

What US Operators Should Watch

Decision-makers should closely monitor the UK economic policies and any shifts in construction demand. Particular attention should be paid to federal deadlines and procurement opportunities in the energy sector, which remains a bright spot amidst the broader downturn. Additionally, tracking input cost trends and supply chain developments will be essential for maintaining competitive positioning and optimizing ROI.

Is your firm ready for what’s next?

VisioneerIT helps AECM and government contractors modernize operations, achieve compliance, and implement AI.

Explore VisioneerIT Solutions →Tracking the right federal opportunities?

OryonIQ's AI platform monitors agency forecasts, contract awards, and procurement timelines — so government contractors always know what’s coming next.

Try OryonIQ Free →