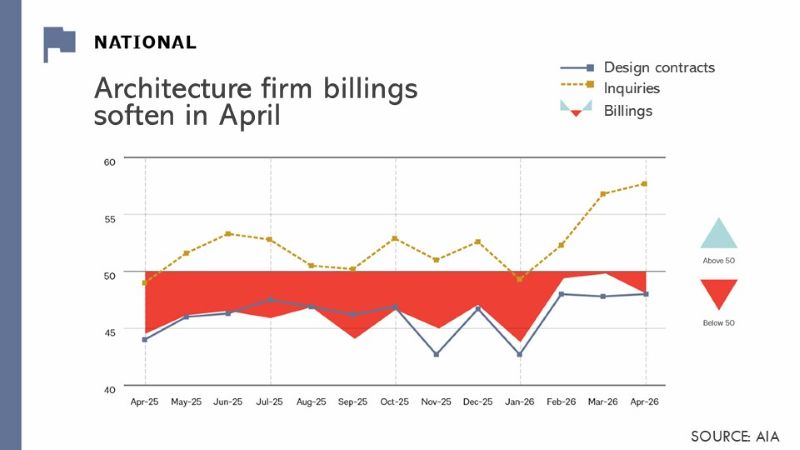

The AIA/Deltek Architecture Billings Index (ABI) recently reported a decline from 49.8 in March to 48.3 in April 2026, highlighting a sustained contraction in billings at U.S. architecture firms. This marks a continuation of a trend where the ABI has not surpassed the growth threshold of 50 since January 2023, indicating a prolonged period of reduced activity in the architecture sector.

What Happened

The ABI, a crucial economic indicator that forecasts nonresidential construction activity 9 to 12 months ahead, reflects ongoing challenges in the architecture industry. With an index score below 50, the data suggests more firms are experiencing a decrease rather than an increase in billings. Despite this, there was a positive note as inquiries into new projects have risen for the third consecutive month, and the value of new design contracts is nearing growth. Regionally, the West showed the most resilience, while the South saw further declines after a brief period of optimism earlier this year. In terms of specialization, commercial and industrial sectors remain weak, whereas institutional and multifamily residential sectors reported modest growth.

Why It Matters for the AECM Industry

For professionals in the architecture, engineering, construction, and manufacturing sectors, the ABI is a vital tool for anticipating market conditions and planning strategically. The ongoing contraction implies potential delays in project pipelines, increased competition for fewer projects, and potential challenges in workforce management. The decline in architectural services employment by 600 jobs in March underscores the pressure on firms. However, the uptick in project inquiries and contracts nearing growth could signal opportunities emerging in institutional and residential markets. Firms need to adapt quickly to these shifts to maintain competitiveness.

What's Next

Industry stakeholders should closely monitor upcoming ABI reports to assess whether the positive trends in project inquiries and contract values will translate into tangible growth. Additionally, firms should prepare for potential shifts in demand, particularly in the institutional and residential sectors. As the industry awaits further data, strategic planning and diversification into more resilient sectors may prove crucial. Firms should stay attuned to regional differences and sector-specific dynamics to na

Is your firm ready for what’s next?

VisioneerIT helps AECM and government contractors modernize operations, achieve compliance, and implement AI.

Explore VisioneerIT Solutions →